What is an Export?

Exports defiance of Goods (Cargo) Movement form load port to destination port on 3 modes i.e by see/Air and land.

What is shipping bill and how many types of shipping bill?

Shipping is a Document Which will be Generated by Customs Authorities against basing on the shipment Documents submitted by the Exporter for exportation of goods - in other words shipping bill represents entire shipping information about the specific shipping details.

Types of Shipping Bills

Duty Free

Incentive Based

Re Export/Return

Duty Free Shipping Means in this Specific Scheme Exporter will be Filing the Shipping bill without claiming any kind of Export Incentive /Reward From Customs And it scheme code “00”

Incentive Based Shipping Bill Means Exporter will be Filing the Documents with Customs against under various Incentive Schemes viz., Duty drawback /Advanced License/EPCG/DFIA/MEIS, etc.

Re Export/Return Means in this specific case during the time of materials Importation by an Exporter will be Importing on condition stating that Exporter will re-Exports the good for supplier for repair purpose.

In case of Return During the time of imputation materials will be imported for a specific cause and on completion of the said cause completion material will be returned to the supplier an exporter.

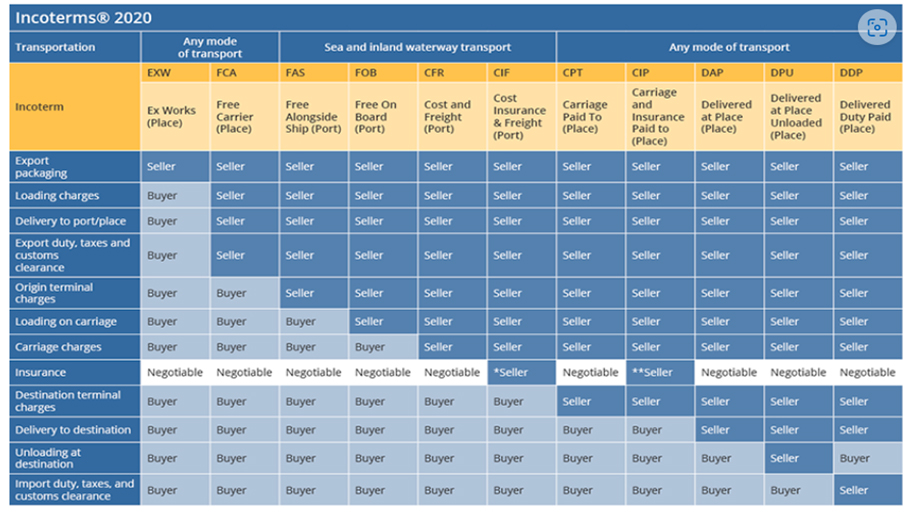

What is INCO Terms?

Inco-terms, widely-used terms of sale, are a set of 11 internationally recognized rules which define the responsibilities of sellers and buyers. Inco-terms specify who is responsible for paying for and managing the shipment, insurance, documentation, customs clearance, and other logistical activities and below is the chart which explains about the responsibilities of the Buyer and Seller.

Who will issue the Incentevies

AS per the policy these incentives will be issued by Joint Director General of Foreign Trade who works under the guidelines of Ministry of Finance and Ministry of Commerce and time – to – time JDFGT will be monitoring various activities of the Exporter and Importer and also supporting Exporters to enhance foreign revenue reserves with the Govt.

Duty Drawback Scheme

Duty drawback refers to the refund of customs duties and internal taxes paid while importing goods, which in turn are used to manufacture final products exported from India. For instance, refund of custom duties and taxes paid on machinery imported that is used to manufacture textile products.

Advance Authorization Scheme

Advance Authorisation Scheme allows duty free import of inputs, which are physically incorporated in an export product. In addition to any inputs, packaging material, fuel, oil, catalyst which is consumed / utilized in the process of production of export product, is also be allowed.

EPCG Scheme

EPCG scheme covers manufacturer exporters with or without supporting manufacturer(s), merchant exporters tied to supporting manufacturer(s) and service providers. To apply for an EPCG scheme, an IEC is required.

SEIS Scheme

Under the Service Exports from India Scheme (SEIS), the Duty Credit Scrips are accorded as rewards. The goods imported against the Duty Credit Scrips or the goods nationally acquired against the Duty Credit Scrips will be transferable freely.

DFIAScheme

Duty Free Import Authorization (DFIA) is issued to allow duty free import of inputs which are used in the manufacture of an export product, making normal allowance for wastage, and energy, fuel, catalyst etc. Many are utilized in the course of their use to obtain the export product.

DFRC Scheme

Duty Free Replenishment Certificate (DFRC)-exemption of basic duty and SAD. Exemption to materials used in the manufacture of resultant products when imported under replenishment Certificate License.

MEIS Scheme

A scheme designed to provide rewards to exporters to offset infrastructural inefficiencies and associated costs. The Duty Credit Scrips and goods imported/ domestically procured against them shall be freely transferable.

RODTEP Scheme

RODTEP is based on the globally accepted principle that taxes and duties should not be exported, and taxes and levies borne on the exported products should be either exempted or remitted to exporters.